WE

ARE ENTITLED TO RELIEF ON INCOME TAX ON OROP-ll

& lll , 7 CPC & PMR ARRs PAID IN THE

CURRENT FY - (2016-17) TO THE EXTENT OF LESSER INCOME TAX THAT WE

WOULD HAVE PAID ON THESE ARRs HAD THEY BEEN PAID TO US DURING THE PREVIOUS

YEARS THAN WHAT WE WILL PAY TODAY.

During the last year our team brought out for

you a post on this very subject, where in we had given a "PRIMARY SCHOOL

SOLUTION" to work out the Relief on Income Tax on such like Arrears and to

prepare and submit FORM 10-E on line while e-filing your ITR under Sec 89(I) of

the IT ACT. This post has benefitted a large number of pensioners in saving

their Income Taxes in thousands. Do read the old post which had detailed

explanations on the method. The webpost is accessible at the web page - http://signals-parivaar.blogspot.com/2016/05/relief-on-income-tax-for-arrears.html

This endeavour

helped a large number of officers who made efforts to DO IT YOURSELF in

claiming their relief, the max being Rs 80,000/- and lowest as much

as Rs 1650. We received many encouraging words from them.

Some Veterans even resorted to filing their REVISED RETURNS to claim the IT

relief after reading our web-post.

Last year we were also informed by veterans they had seen many CAs

referring to our Web Site, while filing returns for their customers

and charging them something like Rs 2500/- where as the same could have, well

been done by them on their own based on the simple primary school method

given in our post. It was also reported by some Veterans from

Meghalaya, Tamil Nadu and Rajasthan that some Cyber Cafe

walas charged as much as Rs 50/- to Rs 100/- for providing information

on Pension Entitlements and OROP referring to our blog site.

We are thus encouraged to bring out this post

which covers the arrears paid during FY 2016-17 on OROP. 7 CPC and Arrears on

DL 33 Yrs Rule (PMR CASES)

WHY THE RELIEF

UNDER SEC 89(1).

Before we proceed

further let us understand the principle under which such a relief is entitled.

You are receiving these arrears late by a year or more as the Govt could not

pay you these amounts during those earlier years for some reasons.

"HAD THESE

ARREARS BEEN PAID DURING THE PREVIOUS YEARS YOU WOULD HAVE PAID TAX AS PER

YOUR LESSER "TOTAL TAXABLE INCOME (T.I)" AND LOWER IT RATES FOR

THAT YEAR, THAN TODAY, WHILE YOU FALL IN THE 30% BRACKET. THIS AMT OF

LESSER TAX AS COMPARED TO THE CURRENT YEAR IS YOUR RELIEF UNDER SEC

89(1)".

Important Note

-- As a thumb rule 'Other than PMR cases' in case, they were taxed at the same

slab (suppose 30%) in the previous two Financial Years ie 2014-15 and 2015-16

as they may be Taxed during the current year "No Relief" is

likely to accrue. However the PMR cases will certainly have adequate Relief

available to then which could be over One lakh of rupees in some cases.

Let us now proceed to deal with the arrears as received

during the last Financial years i.e. FY 2016-17. During this

financial year mainly following arrears were received by us :-

* Second Installment of OROP.

* Third Installment of OROP.

* 7 CPC Arrears.

* PMR CASES (DL 33 Yrs Rule) - Arrears.

HOW TO ACCOUNT FOR OROP INSTALMENTS

1. Total Arrears on OROP

so accrued wef Jul 2014 till Feb 2016, when the OROP was

paid were divided into four portions. The FIRST one was paid

in Feb 2016 (FY 2015-16) , the SECOND one in Aug 2016 (FY

2016-17) and the THIRD too has been paid in March 2017 (FY 2016-17) in most

cases. These arrears infect pertain to the period starting from 01 July

2014 to 31 Dec 2015 for Relief purposes. These can be easily

split for two years ie FY 2014-15 and 2015-16 to claim relief.

2. One needs to know the increase/Hike in basic pension

on OROP from the 6CPC figs are required to proceed further. The Table No, 1 on

the right gives these figures for various ranks with full QS. In addition one

also needs to know whether the relief was claimed on first installment in

the last IT-Return for FY 2015-16 (Ass Yr 2016-17), showing it as

arrears of the previous FY 2014-15. If not then the same was

obviously included in the Total Taxable Income for the FY 2015-16 and tax paid.

3. In order to split the arrears we have derived

the magic MF (Multiplication Factors) on the hike on basic pension to arrive at

various figures for distribution of these OROP arrears to earlier FYs for

all ranks. The hike will be different for different pensioners but the MF

remains the same. Please see the calculations as below as your guide:-

* FY 2014-15 (MF=18.81) : for a Lt Col

the increase is 34765 minus 26265 = 8500 as can be seen in the table here. The

arrears thus work out for the FY 2014-15 as = 8500X18.81 = Rs 159885/-.

Note : In case one had

shown the first installment during this FY and had claimed the relief

under Sec 89(1) the same be deducted from the above total of Rs 159885. The

remaining amt still pertains to this FY and can be claimed for relief

from the second installment.

* FY 2015-16 (MF - 26.28) ; Here again for a Lt Col the arrears will be = 8500X26.28 = Rs 223380/-

Note : The arrears on OROP received during the current Financial Year

can accordingly be claimed for previous arrears if beneficial. The ready

reckoner for various ranks is placed below:-

|

|

TABLE No, 2 SPLITTING OF OROP ARREARS

|

NOTE :

1. These figs are based on OROP having been received after Mar -

2016. However individual cases should work out differently in case the OROP had

been started earlier. The relief will be permitted on the above figures since

wef 01 Jan 2016, the 7 CPC had been implemented and arrears paid later in 2016.

2. The first installment of OROP was paid mostly in Mar 2016 ie during the FY

2015-16 but actually pertained to FY 2014-15. In case the officers did not

claim any relief on IT on OROP First Installment last year , they can

now show the Second Installment and a portion of the third installment as the

Arrears pertaining to FY 2014-15 and tax relief worked out and claimed..

3.

However in case this instl was shown for FY 2014-15 in last

years' ITR for tax relief, then the balance arrears ie a portion of

Second installment still pertains to FY 2014-15. In this case

portion of Second installment which may be worked out in individual cases can

still be treated as arrears for FY 2014-15 and relief claimed. The remaining

portion will fall as arrears for FY 2015-16. Your own figures will vary

depending upon the hike in OROP

ARREARS

OF 7 CPC SCALES.

1. The 7 CPC was implemented wef

01 Jan 2016 while we all were in the receipt of basic scale of OROP Pension

plus DR @ 125%. The 7 CPC award for every one for the time being has been fixed

at your pension as on 31 Dec 2015 multiplied by a factor of 2.57. The Dearness Relief on this under 7 CPC

was NIL from Jan to Jun 2016 while it has been 2% from Jul to Dec 2016

and 4% from Jan 2017 onwards. It is thus evident that

arrears received on 7 CPC award mostly pertain to last FY-2016-17,

leaving those for Jan to Mar 2016 which pertains

to FY 2015-16 for claiming relief under Sec 89(1). One can thus easily

know this portion of the arrears which pertains to the last year

based on your basic OROP scale as on 31 Dec 2015.

2. * FY

2015-16 (MF = 0.96) : Multiply the OROP basic pension with

this MF to get the arrears. eg Lt Col :: 34765X0.96= 33374.

MF is constant and can also be used for all.

3. To help our readers we are giving a ready reckoner below rank wise

Arrears for three months pertaining to FY 2015-16 to work out and claim rebate.

|

|

TABLE No, 3

SPLITTING OF ARREARS ON 7 CPC

|

NOTE : Add these

arrears to OROP arrears as worked out above for the FY 2015-16

for claiming relief.

1. We received many mails from

pensioners specially from Indian Air Force and Indian Navy who took PMR and are

now entitled to arrears received during the Financial Year,

asking us to help them with relief by doing special web post for the

treatment of arrears received by them on DL33Yrs Rule. This post is in response

to their desires.

2. Most of the PMR

Pensioners have received these arrears before 31 Mar 2017. They must have

already checked the correctness of their arrears based on many tables which had

been circulated on mails by many officers. These arrears pertain to the period

from 01 Jan 06 to 30 Jun 2014, as such the total arrears received on

this account should first be broken down Financial Year wise ie

to the years they pertain.

|

|

TABLE No, 4 SPLITTIMG OF PMR ARREARS

|

3. The total PMR

arrears received by various officers depend on the hike in the basic

pension as affected by the provisions. They should refer to PCDA(P)

Circular No 500, (Circular No 24 – Medicos) and check the hike in

their basic per month pension. this be noted.

4. One can split

the total arrears either by taking into account the monthly hike (using MF as shown under

Coln 'c' of the table No.4 placed alongside - in

this example we have taken Rs 2270/- as the monthly hike in basic pension

amounting to total arrears received as Rs 325652/- .

5. We can also use

percentage methid by multiplying the total arrears received with yearly percentages given under Coln 'e' of

the table above. Coln 'f' thus gives the breakdown Financial year wise for

calculations to arrive at the relief.

DATA

NEEDED TO PROCEED

We therefore need to know the following data

before proceeding further for the treatment of arrears along with the arrears

of OROP and the 7 CPC :-

(a) . Breakdown of arrears received on PMR, OROP and 7 CPC as

described above.

(b) The“TIs” for the Fin Yrs from

2005-06 on wards till Fin Yr 2015-16, to be noted from the ITRs of previous

years correctly. Relief claimed earlier during the previous year for arrears on

Enhanced Pension, OROP Etc for the each previous year. (d)

Form 10-E (Table) of the previous year where the relief on earlier

arrears had been claimed in ITRs.

6. We are now ready to prepare

the Form 10-E for which a Primary Class methodology is given in

our last years blog post. This form will give you the relief

you are entitled now.

MAGICAL

CONSTANTS - MULTIPLICATION FACTORS.

In order to help

our readers in their calculations of pension, arrears etc these Mathematical

Constants, we call them MFs (Multiplication Factors) have been derived from

complicated tables and calculations so as to bring the calculation of arrears

for various periods depending on the Rates of Dearness Relief prevailing from

time to time in this post, to a PRIMARY SCHOOL MATHS problem.

The MFs for various periods are

listed below, you donot have to refer any charts of the DA rates or the

calendar just multiply the hike by the MF for the period and you get the amount

of the arrears, so simple isn't it.

a. 01 Jan 06 to 30

Jun 09 - 46.02

b. 01 Jul

09 to 23 sep 12 - 75.62.

c. 01 Jan 06 to 23 Sep

12 - 103.64

d. 24 Sep 12 to 31 Dec

15 - 78.08

e. 01 Jan 06 to 30 Jun

14 - 143.404

f. 01 Jul 14 to 31 Dec

15 - 38.34

g. 01 Jan 16 to 29 Feb

16 - 4.50 (DA 125%)

Use these MFs for calculating your arrears for

the periods shown, The error which may be there is only an ignorable

fraction in its percentage.

LIVE

EXAMPLE - LT COL XY ZULU (PMR 22.5 YRS QS)

you will need details in respect of your pension and

arrears before you proceed further to file your ITR and claiming relief similar

to what is explained in the succeeding live example.

Let us now work for our

friend Lt Col (TS) XY Zulu, his DATA being:-

a. Date of Birth = Apr 1947, (Hence becomes Sr Ctz

wef in FY 2011-12)

b. PMR after 22.5 yrs of service,

c. Initial pen fixed as on 01/01/06 = Rs

21417/- against Rs 25700/-.

d. Pen under Cir No 500 =Rs 21888/- against

full Rs 26265/- wef 23/09/12 later made

applicable vide Cir No 548 wef 01/01/06.

e. OROP entitled wef 01/07/14 8500/mth = Rs 32428/- against full QS OROP of Rs 34765/-, HIKE

of rs 8500 per month.

f.

Pension fixed under 7 CPC (2.57 times) = Rs 83340/- wef 01/01/16.

g. Total Arrs recd = Rs

892437/- along with his pension making his Total Taxable Income (TI) after

all deductions to Rs 1907517/-.

h. Income Tax on Rs 1907517/- = Rs 4,04,023/- if relief not claimed)

j. Sub-Details of Arrears recd in FY

2016-17 totaling as Rs 892437/- :-

*

Sec installment of OROP = Rs116823/-

* Third Installment of OROP = Rs 116823/-

* 7 CPC Arrears for

Jan, Feb & mar 2016 = 31131/-

* PMR Arrears = Rs

627661/- .

LET US SEE IF OUR FRIEND CAN SAVE ON HIS INCOME TAX BY AN AMT OF OVER Rs ONE LAKH.

Summary

of Arrears Received During Current Year :-

a. OROP-ll

& OROP-lll each = Rs 116823/- (TOTAL =233646)

b. 7 CPC = Rs

31130/- FY 2015-16

c. PMR = Rs

627661/- for Pd Jan-06 to Jun-14

d Normal Pension 2016-17 =

1015080 & Arrs above = 892437/-

TOTAL

= 1907517/-

These arrears are to be further be split

into year wise to which they pertain in accordance with the method explained

above as under:-

a. OROP FY - 2014-15 - HIKE(10540)*18.81= Rs 198258/- (We

presume that First Installment

of Rs 116823 was claimed for relief FY 2014-15 thereby remaining Rs 81438/- out of the two installments amounting

to Rs 233646/- will be claimed again this year.

b. OROP FY - 2015-16 - HIKE(10540)*26.88= Rs 276991/-. Of this only

two installments amounting to Rs 233646 were received in current year as such

they less Rs 81438 ie Rs 152208/- be

shown against FY 2015-16.

c. 7CPC FY -

2015-16 - OROP(32428)*0.96 = Rs 31130/-.

d. PMR Arrs Ttl HIKE (26265-21888)*143.404 = Rs 627661/-.

NOTE - The PMR arrears as above should now be broken down FY wise by method

of percentage as explained above under breakdown (TABLE No, 4). The figs

worked out are shown below. You are now ready to proceed for knowing the relief

if any. Red Figs are inserted in the final chart (TABLE

No, 6).

BREAKING DOWN OF PMR ARREARS (TOTAL = Rs

627661) FY wise

|

|

TABLE No, 5 -SPLITTING OF PMR ARREARS FOR COL

ZULU

|

Now prepare your preliminary data chart based

on above calculated figures as per under mentioned format (TABLE No, 6). PL

DONOT BE AFRAID OF MANY COLNS IN THIS TABLE, SPECIALLY IN CASE YOU DID NOT

CLAIM ANY RELIEF EARLIER, IN THE END you will only need two columns H

& M to proceed further. Fill the above details and your T.I's for the

previous years as per your ITRs filed in earlier years in the following

chart/table (TABLE No, 6):-

TABLE No, 6 (YOUR DATA)

|

|

TABLE

NUMBE - 6 - YOUR DATA CHART

|

NOTE :: Ignore the columns

of earlier claims ie coln "D" to "G" in case not claimed ,

here "C" & "H" will have same values.

You are now ready to

prepare your FORM 10-E which will be submitted on line while filing your

return. In this you need to calculate Income Tax year wise on the

Original/Modified Taxable Incomes with and without the Arrears incl the current

year. For this purpose to your convenience we have placed here the income tax

rates and the slabs pertaining to the earlier years in Table No, 7.

FORM 10 E -Preparation and Submission

While the relief amount will be

reflected by you in the appropriate field in the ITR Form where the amount of

relief will get deducted from the total Tax, the pensioners are required to

submit FORM 10 E on line in support of their relief claimed from the arrears.

This form is of two pages as shown below

(TABLES 8, 9 & 10).

Page one is the summary

and verification from the pensioner.

Page two is "Annx

-1" which contains Particulars and Table A which simply tabulates

the calculations made by you on piece of paper as mentioned earlier. These are

shown below in TABLES 8, 9 and 10 reflecting the case of Lt Col

Zulu.

Let us

help you with one of the years say FY 2011-12 for Table A of the Form 10E, you

will be able to work for other years without any hassle.

Till FY 2010-11 Col Zulu (Apr 1947 born) was under 65 yrs of age as

such not yet a senior citizen. The Sr Ctz age was reduced to 60 yrs wef

FY 2011-12. Our friend therefore is Sr Ctz for Tax purposes wef FY 2011-12 as

such his Income Tax slabs & rates for the FY 2011-12

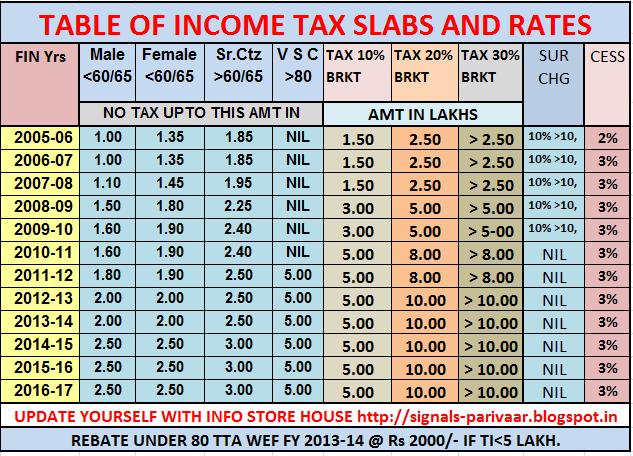

applicable will be as can be seen in the Table No, 7. :-

No Tax upto 2.5 Lakh of TI,

10% 2.5 L to 5 Lakh,

20% 5 to 8 Lakh &

30% >8L

The T.I (Table 6) for FY 2011-12 is Rs 464996/- and the arrs of assigned

for this year are 82988. Now calculate the Income Tax first for Rs 464996/-

(w/o arrs) which works out to Rs 22145/- and for Rs 547984/- ie with arrs

(464996+82988= 547984) tax works to be Rs 35635/- ie Rs 13494/- more

than what it is without arrears. These values

are inserted in Table 'A' of Annx-1 of Form 10 E (TABLE-9) placed

below.

Similarly work out the Taxes and difference for

all other years and complete the Table A of Annx-1. Once done You

have won the battle for yourself.

INCOME TAX RATES - TABLE No, 7

|

|

TABLE

NUMBER 7 - INCOME TAX RATES

FORM 10-E - PAGE 1

This is the

beginning part of the form 10 E which will appear on line once you ae in the

process of on line submission of this form. Here one only needs to

specify the Total Arrears being assigned for earlier year. This can be even

less than the total arrears received by you as you are at liberty to claim

for arrears which are more beneficial to you.

|

|

TABLE

NUMBER - 8 - FORM 10 E PAGE 1

|

|

TABLE 'A'- Part

of Annex 1

This table is by far the most important showing the

difference in income tax that you would have paid for all the previous years

for the arrears had they been received by you during the previous year rather

than the current year. The details of working out has been explained above. The

figures given in this table by you must be accurate, since these are checked in

the Dept with your earlier ITRs.

Prepare this \Table and use the same for on line completion while submitting

the Form 10-E along with your ITR.

|

|

TABLE

NUMBER - 9 - TABLE A OF ANNX-1 OF FORM 10-E FOR ON LINE SUBMISSION

SLABS TAKEN--

In

the above Form for the years shown are the Financial Years . The subject

assessee became senior citizen during the FY 2011-12 as such his calculations

from the said FY on wards are based on slabs prescribed for

a Senior Citizen and calculations before 2012-13 are for MALE Assessee.

Once the above table has been made, your

battle stands won by you, what remains is minor completion of columns of

Annx-1 on line as below.

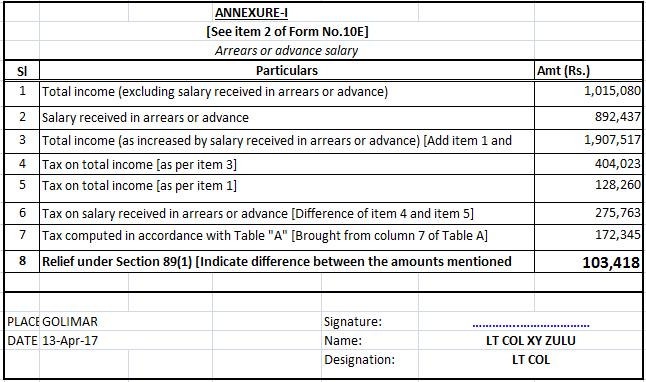

ANNX -

1 OF FORM 10-E , GIVING THE AMOUNT OF RELIEF UNDER SEC 89(1) - TABLE NUMBER

-10

Here on Table- 10 we insert the income (1015080) and

the arrears (892437 ie Only up to the extent being assigned to previous

years) of current year. The total becomes 1907517 (Tax Calculated on this

amount is Rs 404023/-) while the Tax on income w/o arrs ie Rs 1015080/-

is calculated as 128260/- . Hence the diff in Tax on income with and

w/o arrs for the current year (Ass Year 2017-18) is equal to Rs 275763/- .

Deduct from this the total difference as calculated in Table 'A' (table No,

9) to obtain the amount of relief which is Rs 1,03,418/- a substantial

amount for Zulu to take his family for a Hoilday.

|

|

|

TABLE

- 10 - ANNX 1 OF FORM 10-E FILLED UP FOR ON LINE SUBMISSION

|

ON LINE UTILITIES -

There are many on line applications available launched by

various establishments which file ITRs on behalf of their clients on payment.

They are simple to use and need only filling up the arrears spitted as per past

years and the applications does all calculations for you and also produces Form

10 E. One can make use of them as well if one can however care should be taken

that the calculations are for the age of the assessee. Any mistake if made in

the Form the responsibility will be of the assessee and the Income Tax

Department may not admit the Relief because of these errors. It will be

worthwhile to recheck the outputs by manually calculating as well.

E-FILING OF ITR AND ON

LINE SUBMISSION OF FORM 10

ITR - First after you have calculated your data you

may prepare your ITR for efiling based on On line Forms ITR-1 or as applicable.

These forms has a field to insert the Total amount of Relief claimed. This

amount gets reduced from the over all tax liability.

FORM - 10 E - The

E-filing site https://incometaxindiaefiling.gov.in caters for on

line filling of the form and submission. One can prepare the form on line and

save it as draft while you are partially ready and finalise later. After you

have logged in with your PAN number and password to your account with them

Click on "e-File" (Refer to following screen shot) select

prepare and submit Form on line from drop down, the screen as below will

appear. Put in details and continue thereafter as per instructions which pop

out,

|

|

FIGURE NUMBER-11 - SCREEN SHOT OF E-FILING

SITE

|

NOTE:- Once again its a simple

affair, the form can be opened on line on e-filing site of the IT Dept

after your own logging in, filled up with your data as worked above page wise

page and submitted on line. You get a confirmation of submission.

However please note that the years as they appear there on their site on

line are assessment years and not Fin Years.

NOTE - We will appreciate your inputs on the

above POST.

****************************************************************

YOUR OBSERVATIONS AND

COMMENTS PLEASE

Dear Veterans,

1. We at

Signals-Parivaar Portal are ordinary people, as such, do heavily bank

upon inputs from our readers on issues concerning us all. Kindly do add,

comment, point out errors or give your observations on this post or

any other post, which we will much appreciate. Our sole aim is to

improve the posted contents for the benefit of the veterans community at large.

2. We have zero

commercial angle to the extent that we have not allowed Google to insert

advertisements on our blog site that could earn us over Rs 10000/- per month

with our high readership. There are NO - Ego's either or any One-upmanship

with other veterans or their organisations.

3. Kindly post your

comments and observations under the comments on this post, we will much

appreciate your contribution in this regard.

4. In order to avoid

spam and unwarranted or mischievous posts, only such entries will get published

where the Veteran has given his/her RANK, NAME & EMAIL ID at the end

of his/her text. You will agree that we must know as to with whom we are

communicating. We regret that your comments

will not be published in the absence of your mail ID rank and Name.

5. We will do our best

to post our response or get in touch with you on e-mail as quickly as possible

after getting the facts vetted from offrs, JCOs and men who are more

knowledgeable on the particular subject.

With best wishes

Sincerely yours,

Brig Narinder Dhand

(Veteran)